概要

- 米国の株式市場の上昇は、特にAIとテクノロジー分野で過去のバブルとの新たな比較を引き起こしている。

- トレーダーは、大型株からバリュー株へのローテーションに注意するか、他の資産を通じてNAS100またはSP500のエクスポージャーをヘッジすることを検討する必要があります。

- 関税をめぐる議論、米国の決算シーズン、そして今後の中央銀行の講演により、さらなるボラティリティが引き起こされ、金利予想がリセットされる可能性がある。

- 今週発表される米国の消費者物価指数(CPI)と生産者物価指数(PPI)は、インフレと評価に対する感情を形作る可能性がある。

バブルトークが再び最前線へ

バリュエーションに関する議論が再び勢いを増している。S&P 500とナスダックは今年急上昇しており、その上昇の大部分はテクノロジー関連銘柄とAI関連銘柄が牽引している。一部のアナリストは、これらの水準は過去のバブルを彷彿とさせると警告している。

ゴールドマン・サックスの幹部らは、株価上昇は依然として純粋な投機ではなく、利益と成長期待によるものだと主張している。

JPモルガンのジェイミー・ダイモン氏は懸念を表明した。6~24ヶ月以内に大幅な調整が起こるとの予測が出ている。多くの人が株価上昇を予想している一方で、下振れリスクは過小評価されていると警告する声もある。

市場構造:狭く、不安定な高値圏

一つの危険信号は市場の幅広さにある。全体の上昇を支えているのは少数の銘柄だけだ。指数が上昇する一方で、多くの銘柄が低迷すると、幅が狭まる。もう一つの危険信号はテクニカル指標の歪みだ。複数の市場でモメンタム指標が極端な値を示していることは、脆弱性を示唆している。

最近の取引では、米中間の関税交渉がセンチメントを揺るがしています。金曜日には、100%の関税と輸出制限の脅威を受け、S&P500指数は2.7%、ナスダック指数は3.6%、ダウ平均株価は1.9%近く下落しました。この反転は、センチメントがいかに急速に変化するかを示しています。

企業業績、金融政策、そして今後の行方

今後の決算シーズンは、最初の大きなストレステストとなる可能性があります。ガイダンスが期待外れになったり、利益率に圧力がかかったりすれば、市場の見方は一変する可能性があります。

連邦準備制度理事会と中央銀行の講演が触媒として浮上している。ハト派的なトーンはリスク資産を支える可能性がある一方で、タカ派的なサプライズが勢いを削ぐ可能性がある。

さらに、貿易面の要素もあります。中国とのレトリックのエスカレーションは、バリュエーションが既に高騰しているまさにその時に、逆風のリスクを高めます。市場は政策に関するノイズに敏感です。

慎重に行動すれば、上昇の可能性は依然として残っているものの、下値リスクは高まっている。トレーダーはヘッジを重視し、相対力戦略を優先し、モメンタム銘柄への極端な投資は避けるべきである。

注目すべき主要シンボル

- DJ30

- NAS100

- SP500

- VIX

- ARKK

今後のイベント

| 日付 | 通貨 | イベント | 予想 | 前回 | アナリストコメント |

| 10月15日 | USD | パウエルFRB議長の発言 | — | — | 金利政策の方向性に注目。 |

| 10月15日 | GBP | イングランド銀行総裁ベイリーの発言 | — | — | 金利方針のトーンに注目。 |

| 10月16日 | AUD | 豪準備銀行総裁ブロックの発言 | — | — | 発言が豪ドル相場に影響する可能性。 |

| 10月16日 | GBP | GDP(月次) | 0.1% | 0.0% | 価格構造に沿えばポンドにプラス。 |

| 10月16日 | USD | PPI(月次) | 0.30% | -0.10% | インフレ動向の指標。 |

| 10月16日 | USD | 小売売上高(月次) | 0.40% | 0.60% | 成長とインフレの綱引き。 |

| 10月17日 | CAD | カナダ銀行マクレム総裁の発言 | — | — | 金利政策発言に注目。 |

今週の主要動向

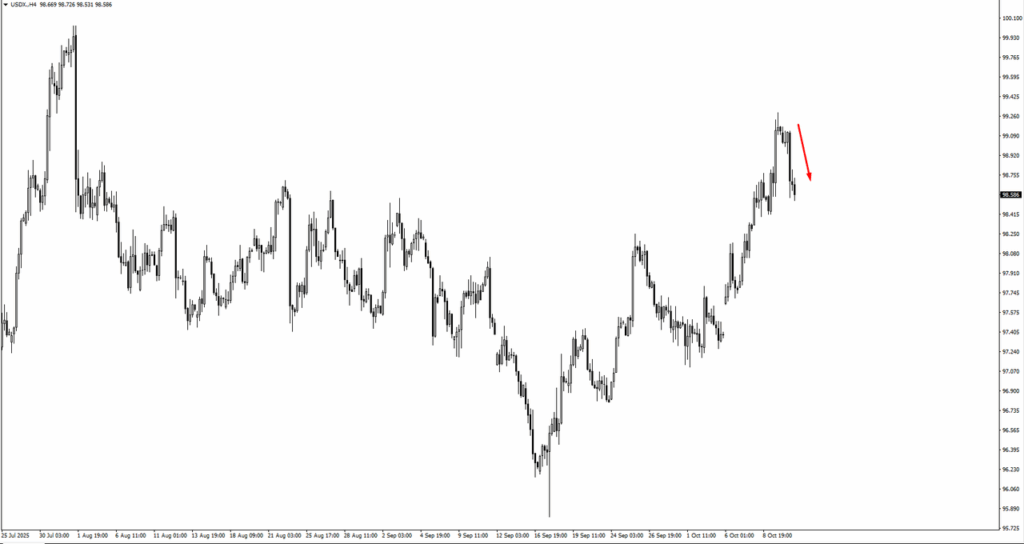

米ドル指数(USDX)

- ドルは98.90~99.00から後退し、先週のレポートで監視されていた抵抗ゾーンと一致した。

- 現在、サポートは 98.20 付近にあり、下落の勢いが続く場合、次の下降目標は 97.90 になります。

- バイアスは98.90を下回って弱気のままです。トレーダーは再参入する前に98.20〜98.70の間の統合に注意する必要があります。

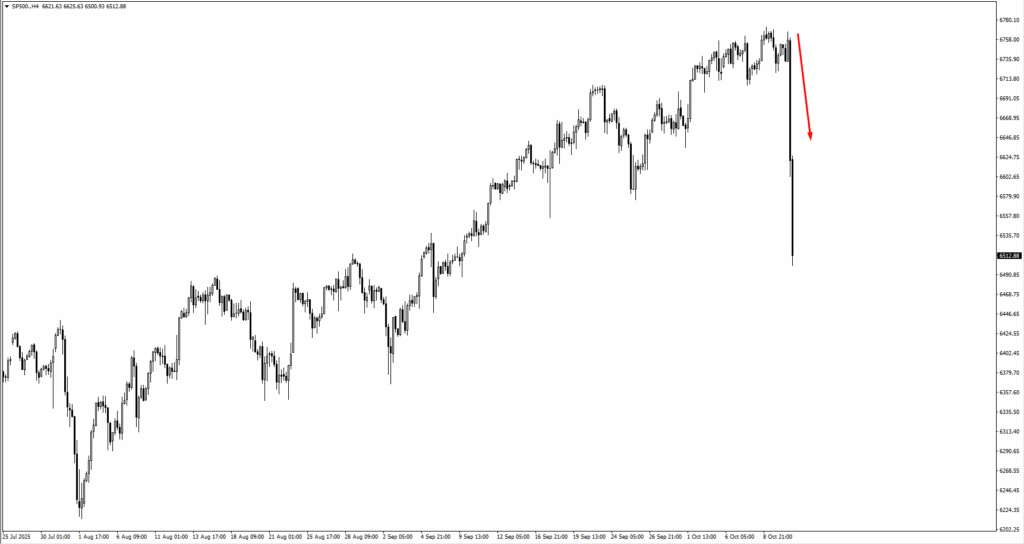

S&P 500(SP500)

- 指数は監視されている抵抗線6,750から崩壊し、リスク回避の流れが強くなり、6,510に向けて急落した。

- 勢いは 6,600 ~ 6,620 を下回ると弱気のままです。次の下降ゾーンは 6,440 と 6,395 付近にあり、後者は監視対象エリアと一致します。

- 短期トレーダーは、6,600 への上昇で株価が落ち着くのを期待するかもしれない。6,660 を完全に上回った場合にのみ、圧力が緩和されるだろう。

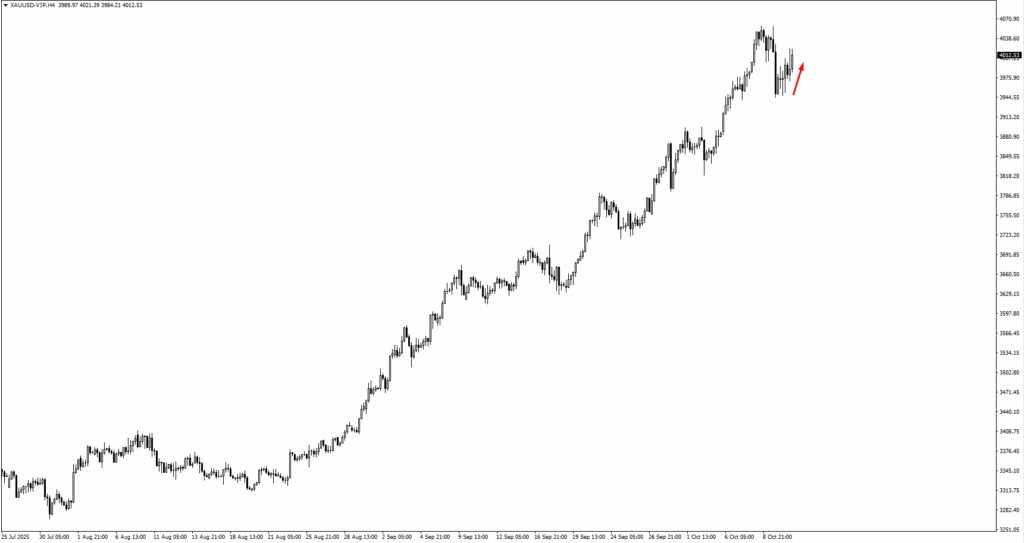

金(XAUUSD)

- 価格は急上昇後、4,010 付近で一時停止し、H4 では 3,985 ~ 3,995 を上回って推移しました。

- 3,980 を超えるとバイアスは上向きのままです。4,045 を突破すると、4,080、そして 4,100 に再び焦点が当てられるでしょう。

- 戦略: 抵抗線に入ると規模を控えめに抑え、3,990~4,010 の安値でリスクを抑えて買い、3,980 を下回ってきれいな終値になった場合にのみ売りを控える。

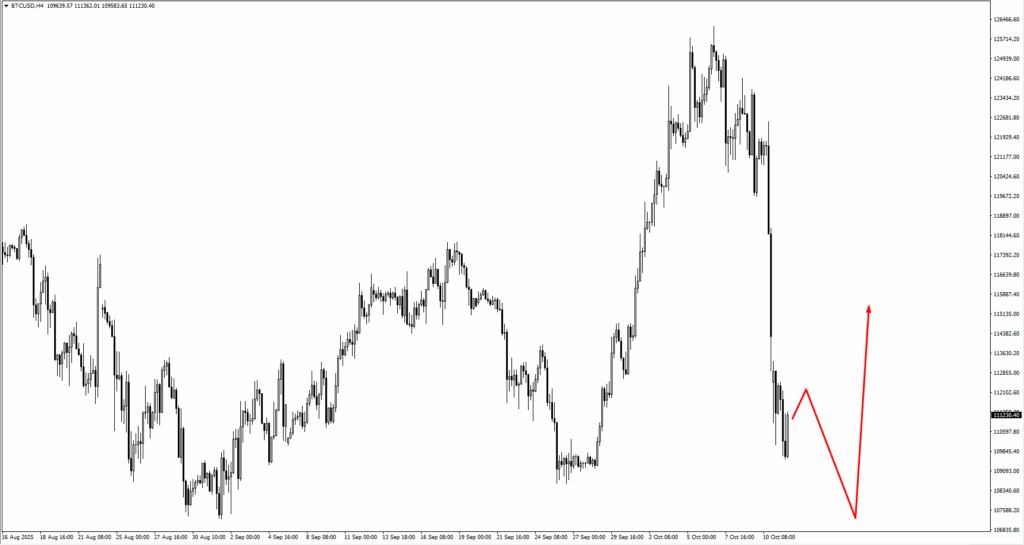

ビットコイン(BTCUSD)

- ビットコインは122,700から急落し、109,600付近の安値に達した後、111,200付近で安定した。

- 短期的な構造としては、108,600~107,240がサポートとして維持され、監視ゾーンと一致する場合、反発が有利になります。

- 慎重な見方が維持されます。日中は113,000~115,000への反発が予想されますが、持続的な回復はより広範なリスク感情に依存します。

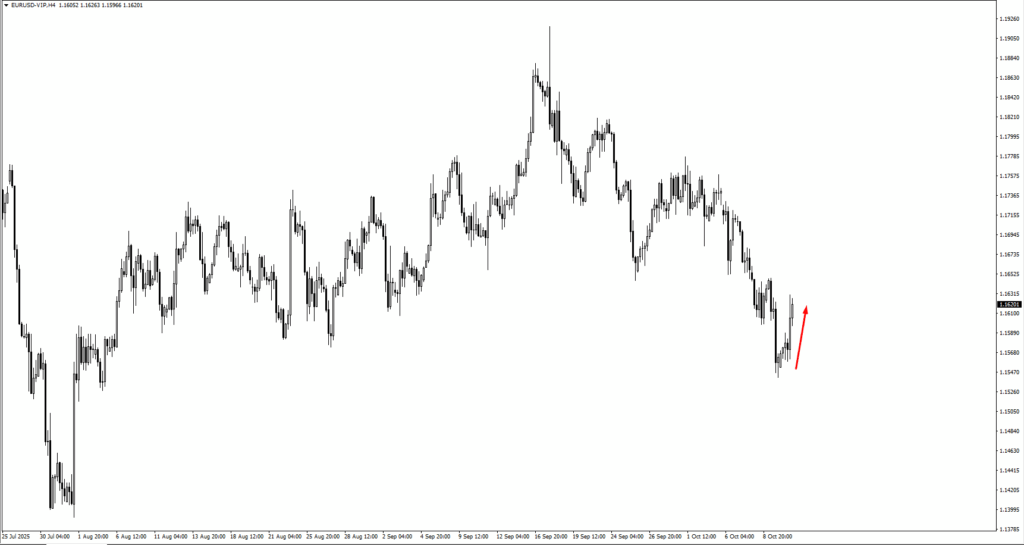

ユーロ/米ドル

- EURUSDは1.1620付近で安定し、1.1580~1.1600の監視サポートエリアから反発した。

- 短期的なバイアスは1.1660に向けてやや強気になり、この水準を完全に上抜ければ1.1700まで上昇する可能性があります。

- 1.1580~1.1660の間での統合に注意してください。1.1580を下回ると、1.1520への道が再び開かれるでしょう。

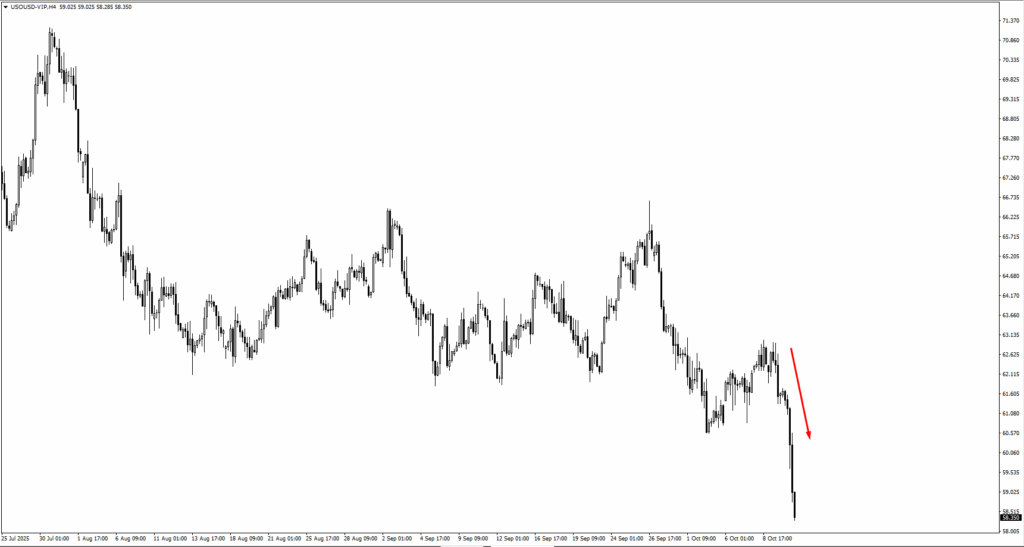

米国石油

- 原油は下落を続け、監視レベルの60.55を下回り、現在はサポートレベル58.35をテストしている。

- 58.00 を超える水準での統合が失敗した場合、レポートに記載されているように、価格は 53.00 付近の次の重要な領域に向かって下落する可能性があります。

- 短期的な反発は59.80~60.50付近で抵抗に直面する可能性があります。60.55を下回るとトレンドは弱気傾向を維持します。

結論

- 割高な評価と狭いリーダーシップの中で、米国株式バブルのリスクが再び注目を集めている。

- 関税リスク、収益ショック、中央銀行の姿勢が急激な変動を引き起こす可能性がある。

- ヘッジされたポジション、選択的なエクスポージャー、テクニカルの尊重は、勢いを追いかけることよりも重要になります。

ライブ VT Markets アカウントを作成し、今すぐ取引を開始しましょう。